Often, a question doesn’t have an easy answer in the digital advertising business. This is a new column devoted to an answer to a single question – and providing a bit of space for it.

Often, a question doesn’t have an easy answer in the digital advertising business. This is a new column devoted to an answer to a single question – and providing a bit of space for it.

Today’s participant is Tolman Geffs, Co-President of Jordan, Edmiston Group, which provides investment banking services in the media and information industries. He recently answered the following question during a conversation with AdExchanger.com…

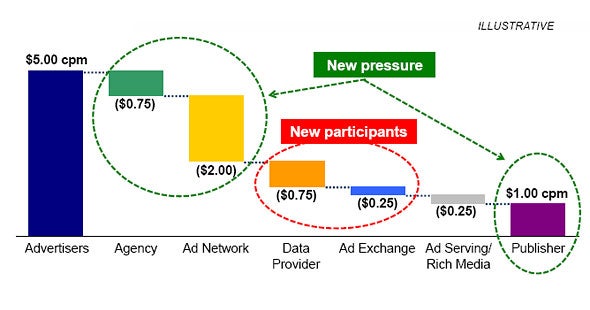

AdExchanger.com: From the Internet Advertising Bureau annual meeting over a year ago, you offered a slide which showed all the slices being taken from the marketing dollar before it ever gets to the publisher. How are the “slices” in the marketing dollar evolving today?

TG: I think right now the chain is even more fragmented. Pricing is even more opaque – particularly with the separation between data and inventory and a more robust market for both. The $1-to-$5 spread can be even wider now than a year ago.

Simply put, publishers are willing to sell “remnant” inventory for a $1 or similarly low CPM. To often, “remnant” means “what our sales team did not know how to sell” rather than “audience that no marketers value”. Ad networks and other intermediaries are able to associate those impressions with desirable audiences using user data and tracking cookies, delivering those to advertisers who are willing to pay something on the order of $5 or more for that user. While difficult to broadly measure, our view is that this spread has if anything been widening – publisher pricing for second tier inventory remains soft while the ability of intermediaries and agency trading desks to package desirable audiences based on user data has been accelerating very rapidly.

One is that publishers are slowly – and I emphasize slowly – becoming aware of the value of their data. I’ve joked that they’re like little old ladies walking down the street with dollar bills fluttering out of their purse. They’re not aware of the value of the data they’re giving up, let alone how to manage it, set rules around it, and monetize it. And monetize doesn’t mean put it up on an advertising exchange and sell it to anybody who wants it. It means to extract value from it under certain rules. That’s shifting, but it’s shifting slowly.

The other tidal force that is coming is that some very big players are building businesses here, and it’s not just Google and Microsoft. People like Experian and Alliance Data Systems in their Epsilon division, and Acxiom – people who make a living handling massive amounts of data on behalf of large marketers and are doing so at very efficient margins. They’re looking hard at how they play in this space.

Other new competitors have emerged – such as Adobe which has been clear they want to play a greater role in the display business. And with that competition and scale, you will see more efficiency and transparency coming back into the system.

So there are a couple of tidal forces at work, but right now it’s like the tide rolling back and forth across the rocks in the harbor. There’s a lot of turmoil.

Follow Jordan, Edmiston (@JordanEdmiston) and AdExchanger.com (@adexchanger) on Twitter.

{kind=link}